As mentioned in our previous article, HSBC Life Wealth Harvest has a diverse selection of over 90 unique investment-linked sub-funds from a range of industries and geographical sectors. From these 90 ILP Sub-Funds, you get to choose one or up to ten. But what do Investment-Linked Policies (ILPs) stand for?

Understanding ILPs

ILP is a hybrid financial product that provides both life insurance and wealth accumulation. With an ILP, your premiums are used to purchase units in one or more sub-funds of your choice. These funds are managed by reputable fund management companies such as EVOL Investment Managers.

Once you have purchased an ILP, units in the sub-fund will be sold to pay for insurance, administrative charges and other costs. What this means for you is that you won’t have to pay separate premiums for the life insurance provided because the units in your sub-funds are already doing it for you.

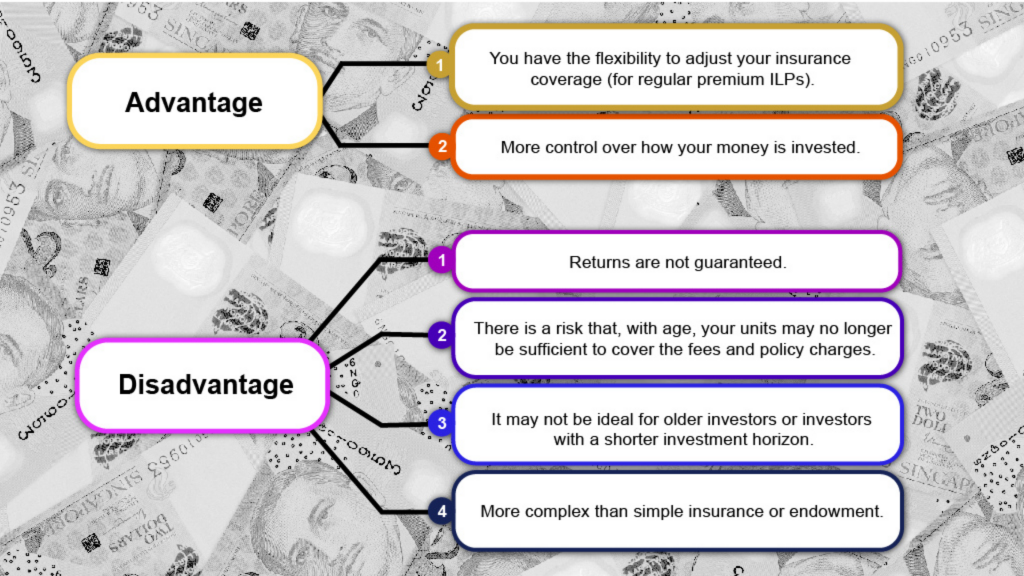

ILPs offer basic life insurance and provide insurance protection in the event of death or Total Permanent Disability (TPD). However, some ILPs cover more. This differentiates it from term life insurance that covers only death and disability without other payouts. Although returns are not guaranteed, ILPs can help you grow your wealth faster than the usual fixed deposits or savings accounts.

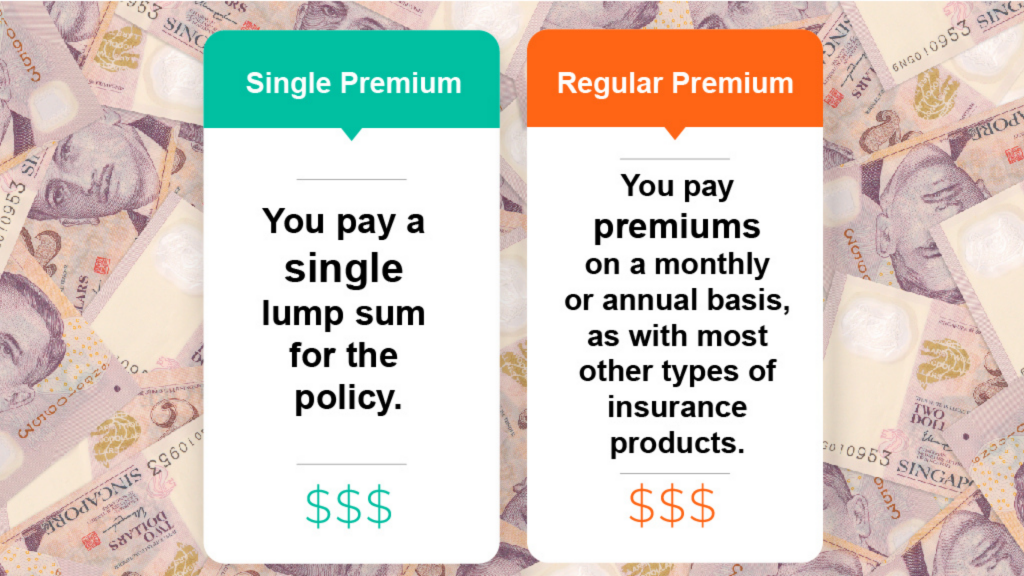

Types of ILPs

Pros and cons of ILPs

How to choose funds?

Pay attention to the risk rating of the sub-fund

Each sub-fund offered will have a risk rating, ranging from low to high. You will need to consider if the sub-fund matches your risk profile and risk capacity—whether or not you are financially able to take on the risk. When choosing your sub-funds, avoid picking purely high-risk or low-risk sub-funds. Instead, make up a good range, from low to medium to high-risk assets.

This is because choosing too many high-risk sub-funds can eat up a lot of your investment in case of a downturn and too many low-risk sub-funds can cause your ILP to underperform and yield lower returns.

Aim to pick a range of sub-funds with low correlation

As mentioned above, HSBC Life Wealth Harvest has a diverse selection of over 90 unique investment-linked sub-funds from a range of industries and geographical sectors. These sub-funds can be divided into geographical region, its commodity type or asset types.

With a variety of selections, your sub-funds should be wide and have a low correlation with one another. This is to avoid both sub-funds from falling in tandem and affect your investment. However, if you are not sure of how to choose a diversified mix of sub-funds, it is best to get professional advice from your financial advisor.

Evaluate the fund’s performance over time

You will also need to constantly check the sub-fund’s performance in over 10 years, instead of just observing its recent performance. This is to give you a more accurate picture of how the sub-fund has been performing and, in turn, help you make the right decision.

Here’s what Joan, our Associate Manager has to say about choosing funds

Speaking from her eight years of experience in the financial services industry, Joan saw some common mistakes people usually make when choosing funds. These mistakes are

Funds not matching risk profile

For example, the client’s risk portfolio is Moderate Aggressive but more than 50% of their funds are invested in fixed interest funds. This has led the clients to not achieve their investment goal with their investment portfolio

Funds are too diverse

Although diversification is important for investment, do know that funds that are too diverse may dilute the investment return.

Failure to review funds portfolio

Most clients just leave their funds without any management. And when this happens, the funds may adjust their investment strategy to those that do not match the client’s investment goal. The manager may also change and this could cause inconsistent investment return. It is better to review the funds bi-annually or annually to make sure the returns are in line with the client’s investment goal.

To avoid making these mistakes, Joan stresses the need to match your risk profile with the funds that you choose and to be very clear of your investment goals. For instance, you must know why you invest, what is the goal that you would like to achieve, how long do you plan to invest and what is the worst result that you can afford.

Nowadays, Environmental, Social, and Governance (ESG) investing has gone mainstream as it offers a way for clients to invest in funds that consider environmental, social, and governance issues. This way, clients can reflect their values through investment to make the world better.

If you’d like to get more insights from financial professionals, get in touch with EΛOL now. We will help you to determine your investment goals and kickstart your investment plan.